How Blockchain Contracts are Transforming Business Agreements

When most people hear the word blockchain, they immediately think of cryptocurrency. While digital currencies have certainly helped bring blockchain technology into the mainstream, they represent only one application of a much larger innovation.

At its core, blockchain is a technology designed to create trust in digital environments. It provides a secure, transparent, and verifiable way to record information that cannot easily be altered or manipulated.

One of the most powerful applications of blockchain is its ability to transform contracts and business agreements. From freelance work and licensing deals to real estate transactions and global commerce, blockchain contracts have the potential to make agreements faster, more transparent, and more efficient.

As businesses continue their digital transformation, understanding how blockchain contracts work may become increasingly important for entrepreneurs, creators, and business leaders alike.

How Traditional Contracts Work

For centuries, contracts have served as the foundation of business relationships.

Whether hiring an employee, purchasing a property, licensing content, or signing a supplier agreement, contracts establish expectations between parties and provide legal protection when disputes arise.

Traditional contracts often involve multiple steps:

- Negotiation of terms.

- Document preparation.

- Review by legal professionals.

- Signing and execution.

- Storage and record keeping.

- Manual enforcement of obligations.

While this system has worked for generations, it can be slow, expensive, and vulnerable to errors, delays, and disputes.

What Are Blockchain Contracts?

Blockchain contracts are digital agreements recorded on a blockchain network.

Because blockchain records are distributed across multiple computers, the information is highly secure and difficult to alter after it has been recorded.

This creates a shared source of truth that all parties can verify.

Instead of relying on a single organization to maintain records, blockchain allows participants to trust the integrity of the system itself.

Every action is time-stamped, transparent, and permanently recorded, providing an audit trail that can be reviewed at any time.

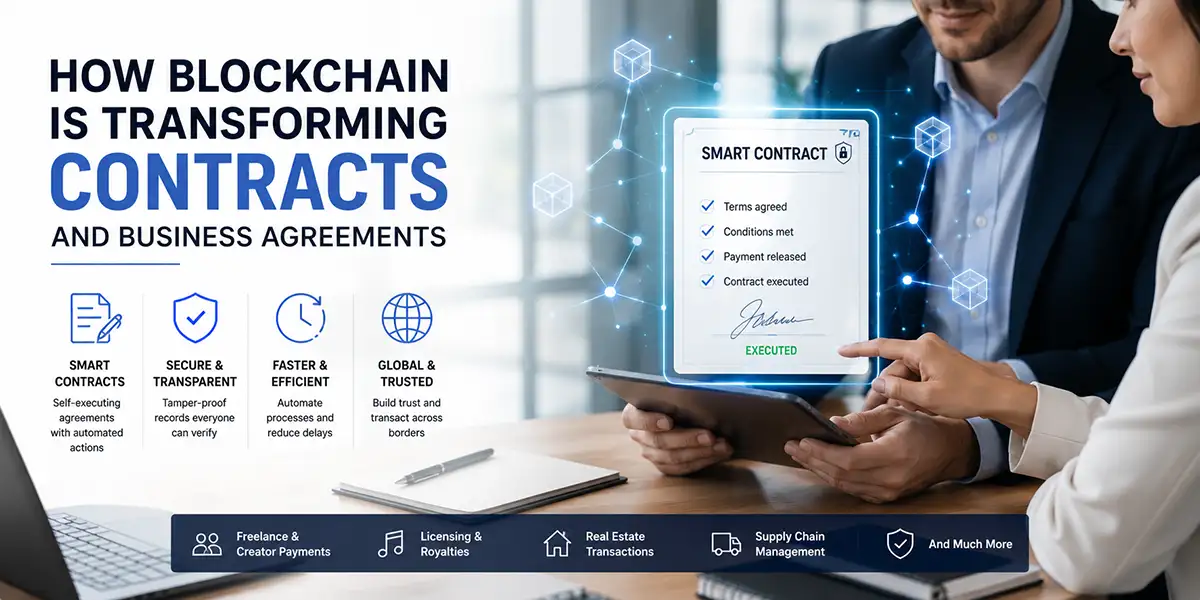

The Rise of Smart Contracts

Perhaps the most revolutionary aspect of blockchain technology is the concept of smart contracts.

A smart contract is a self-executing agreement programmed to automatically perform specific actions when predetermined conditions are met.

The simplest way to understand a smart contract is through an “if this, then that” example.

- If a project is approved, release payment.

- If a product is delivered, transfer ownership.

- If an invoice is paid, provide access to services.

- If a rental agreement expires, terminate access rights.

Instead of requiring manual intervention, the contract executes automatically according to the rules established by the parties involved.

Real-World Business Applications

Blockchain contracts are already being explored across numerous industries.

Freelance and Creator Payments

Creators, designers, developers, and consultants often experience payment delays. Smart contracts can automatically release funds when agreed milestones are completed.

Licensing and Royalties

Music, photography, video, and digital content can be licensed through blockchain systems that automatically distribute royalties whenever content is used.

Real Estate Transactions

Property purchases involve multiple intermediaries and lengthy processes. Blockchain contracts could streamline ownership transfers, payment verification, and record keeping.

Supply Chain Management

Companies can track products from production to delivery while automatically triggering payments or approvals as milestones are completed.

Benefits of Blockchain Contracts

Businesses are interested in blockchain contracts because they offer several significant advantages.

- Transparency: All parties can verify contract activity.

- Security: Records are difficult to alter or tamper with.

- Automation: Smart contracts reduce manual administration.

- Efficiency: Transactions can be completed faster.

- Lower Costs: Reduced reliance on intermediaries.

- Global Accessibility: Agreements can operate across borders.

These benefits make blockchain particularly attractive for digital businesses operating in increasingly global markets.

Challenges and Limitations

Despite its potential, blockchain technology is not without challenges.

- Regulatory uncertainty.

- Legal recognition in some jurisdictions.

- User education and adoption.

- Technical complexity.

- Integration with existing systems.

Many organizations are still learning how blockchain technology fits within existing legal and business frameworks.

As standards mature and adoption grows, many of these challenges are likely to become easier to address.

Why Blockchain Matters Beyond Cryptocurrency

One of the biggest misconceptions surrounding blockchain is that it exists solely to support cryptocurrencies.

In reality, blockchain is fundamentally a trust technology.

Its ability to create transparent, verifiable, and automated systems has implications far beyond financial transactions.

Contracts are simply one of the earliest and most practical examples of how blockchain can improve the way businesses operate.

The Future of Business Agreements

As more business activity moves online, the need for secure, transparent, and automated agreements will continue to grow.

Blockchain contracts and smart contracts offer a glimpse into a future where agreements can execute automatically, reduce administrative overhead, and increase trust between parties.

While widespread adoption may still take time, the direction is becoming increasingly clear. Blockchain technology is evolving beyond cryptocurrency and becoming part of the infrastructure that could power the next generation of digital business.

For business owners, entrepreneurs, and creators, understanding blockchain contracts today may provide a valuable advantage as the future of commerce becomes increasingly digital.